Halifax - Existing Customer Rates 60% LTV

- All

- 2 Years

- 5 years

Type

|

Rate

|

Until

|

Product Fee

|

|

|---|---|---|---|---|

| 2 years Fixed | 3.87% | 31 Jan 28 | £999 | Apply |

| 5 years Fixed | 4.01% | 31 Jan 31 | £999 | Apply |

| 5 years Fixed | 4.22% | 31 Jan 31 | £0 | Apply |

| 2 years Fixed | 4.33% | 31 Jan 28 | £0 | Apply |

| 2 years Tracker | 4.55% | 31 Jan 28 | £0 | Apply |

Halifax - Existing Customer Rates 60% LTV at November 11, 2025

Halifax - Existing Customer Rates 75% LTV

- All

- 2 Years

- 5 years

| Type

|

Rate

|

Until

|

Product Fee

|

|

|---|---|---|---|---|

| 2 years Fixed | 3.98% | 31 Jan 28 | £999 | Apply |

| 5 years Fixed | 4.02% | 31 Jan 31 | £999 | Apply |

| 5 years Fixed | 4.23% | 31 Jan 31 | £0 | Apply |

| 2 years Fixed | 4.44% | 31 Jan 28 | £0 | Apply |

| 2 years Tracker | 4.67% | 31 Jan 28 | £0 | Apply |

Halifax - Existing Customer Rates 75% LTV at November 11, 2025

Please note: Halifax do not have a uniform set of rates for product transfers. Each individual customer is now offered their own set of rates to choose from.

The rates shown are the lowest we have seen currently offered.

Call us on 0208 979 9684 or click here to obtain your personalised list of Halifax product transfer rates

- FREE email alerts

- Upcoming rate changes

- The best mortgage rate

- Protection against rate rises

- No obligation

Halifax - Existing Customer Rates 80% LTV

- All

- 2 Years

- 5 years

| Type

|

Rate

|

Until

|

Product Fee

|

|

|---|---|---|---|---|

| 5 years Fixed | 4.18% | 31 Jan 31 | £999 | Apply |

| 2 years Fixed | 4.22% | 31 Jan 28 | £999 | Apply |

| 5 years Fixed | 4.39% | 31 Jan 31 | £0 | Apply |

| 2 years Fixed | 4.68% | 31 Jan 28 | £0 | Apply |

| 2 years Tracker | 4.72% | 31 Jan 28 | £0 | Apply |

Halifax - Existing Customer Rates 80% LTV at November 11, 2025

Why book your mortgage rate early?

Halifax have a four month mortgage rate reservation window.

It can be a major advantage to book your mortgage rate early. Careful handling by our Team can see you get the best deal possible.

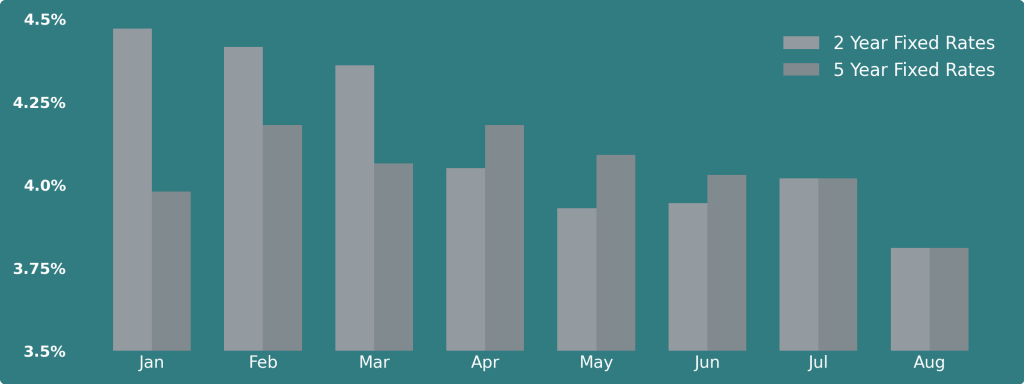

Below is a chart showing the typical lowest mortgage rates offered by Halifax to existing customers in early 2025.

Rising mortgage rates

If you secure a 5 year fixed rate in January to start 1st May you will be better placed than if you wait to secure a rate in March or April when rates have risen.

If you secure a 2 year fixed rate in May to start 1st August you will be better placed than if you wait to secure a rate in June or July when rates were higher.

Falling mortgage rates

Halifax allow you to change your reservation as late as the month before your rate is due to start.

If you secure a 2 year fixed rate in January to start 1st May you would see rates drop in February, March, and April.

Each time our Team can secure the new, lower rate for you.

Halifax - Existing Customer Rates 85% LTV

- All

- 2 Years

- 5 years

| Type

|

Rate

|

Until

|

Product Fee

|

|

|---|---|---|---|---|

| 5 years Fixed | 4.18% | 31 Jan 31 | £999 | Apply |

| 2 years Fixed | 4.22% | 31 Jan 28 | £999 | Apply |

| 5 years Fixed | 4.39% | 31 Jan 31 | £0 | Apply |

| 2 years Fixed | 4.68% | 31 Jan 28 | £0 | Apply |

| 2 years Tracker | 4.85% | 31 Jan 28 | £0 | Apply |

Halifax - Existing Customer Rates 85% LTV at November 11, 2025

Halifax - Existing Customer Rates 90% LTV

- All

- 2 Years

- 5 years

| Type

|

Rate

|

Until

|

Product Fee

|

|

|---|---|---|---|---|

| 5 years Fixed | 4.34% | 31 Jan 31 | £999 | Apply |

| 5 years Fixed | 4.55% | 31 Jan 31 | £0 | Apply |

| 2 years Fixed | 4.69% | 31 Jan 28 | £999 | Apply |

| 2 years Fixed | 5.15% | 31 Jan 28 | £0 | Apply |

Halifax - Existing Customer Rates 90% LTV at November 11, 2025

Halifax standard variable rate is now 7.49% – take action to avoid it

Halifax House Price Index

Halifax house price index and your mortgage options as an existing Halifax borrower.

One of the key parameters that affect your mortgage rate options is the loan to value on your account. This is the ratio of the mortgage balance to the estimated value of the property. The estimated value of your property on the Halifax system is driven by the Halifax House Price Index.

If the Halifax House Price Index falls, your valuation may fall and your loan to value increase. This may push your mortgage account into a new, more expensive set of product options.

The next Halifax House Price Index report is due early in January 2024 and values are likely to be reduced due to current market conditions.

What does this mean for you as a Halifax existing borrower?

The smart approach will be to secure a new Halifax product transfer rate now before any valuation changes. You can secure a new rate up to four months before your current rate is due to end.

Securing a rate now will protect you from adverse valuation changes, or future rate rises.

If Halifax product transfer rates fall between now and when your new rate is due to start, you have the option to pick up the lower rate.

Halifax Product Transfer Rates – Early Repayment Charges

| Product & Term | Period | Charges | End Date |

| 2 Year Fixed | 1 | 2% until 31/01/27 | 31/01/28 |

| 2 | 1% until 31/01/28 | ||

| 5 Year Fixed | 1 | 5% until 31/01/27 | 31/01/31 |

| 2 | 4% until 31/01/28 | ||

| 3 | 3% until 31/01/29 | ||

| 4 | 2% until 31/01/30 | ||

| 5 | 1% until 31/01/31 | ||

| 2 Year Tracker | 1 | 1% until 31/01/27 | 31/01/28 |

| 2 | 0.5% until 31/01/28 |

Overpayment allowances

As a concession, Halifax allows overpayments each calendar year of up to 10% of your outstanding balance without early repayment charges.

If you intend to make regular or lump sum overpayments, first check with the lender that you will be within your overpayment limits.

When can I select a new Halifax Product Transfer Rate?

Halifax existing customers can now select and secure a new Halifax Product Transfer rate up to four months before their current mortgage product ends.

Example: The existing rate ends on 31st December, and a new rate can be selected from 1st September

| Your current rate ends | The new rate can be reserved from | The new rate can start from |

| 29th February | 1st November | 1st December |

| 31st March | 1st December | 1st January |

| 30th April | 1st January | 1st February |

| 31st May | 1st February | 1st March |

| 30th June | 1st March | 1st April |

| 31st July | 1st April | 1st May |

| 31st August | 1st May | 1st June |

| 30th September | 1st June | 1st July |

| 31st October | 1st July | 1st August |

| 30th November | 1st August | 1st September |

| 31st December | 1st September | 1st October |

| 31st January | 1st October | 1st November |

Our Halifax Mortgage Product Transfer Process

- Call our Team, or complete our enquiry form

- Once we have your permission we will email you full details of your current mortgage and your new mortgage options.

- This information will be outlined clearly on a single page.

- You can then consider your options, and we will be available by telephone, text, or email to answer any questions you may have and guide you as necessary.

- Once you have advised us of your preferred option, we will generate a formal Halifax product transfer mortgage offer and email it to you for approval.

Points to note

Our Halifax mortgage product transfer service is free of charge

A mortgage product transfer with Halifax does not require:

Credit searches

Proof of income

Property valuation or visit

Legal work

This means a drop in your income since you first took your mortgage will not prevent you from securing a new rate with Halifax.

You can secure a new rate with Halifax up to four months before your current mortgage rate ends.

If Halifax offered rates improve before your current mortgage rate ends, we can swap you on to the new, lower rate.

If rates increase before your current mortgage rate ends, your secured rate is unaffected.

If requested, we can compare your Halifax rates against options from the whole of the UK market.

A mortgage secured against your home is a regulated product and we will therefore need to gather a little background information in order to progress your rate switch. We gather this information securely online and it will take no longer than 5 minutes for you to provide the required information to us.

Worried about your mortgage interest rate rising?

Please note:

If you are on a fixed rate you are currently safe from BOE base rate rises. Currently, arranged fixed-rate mortgages do not rise with the Bank of England base rate, however, rising BOE rates do put pressure on future fixed rates to rise. Tracker rates will rise immediately with the Bank of England base rate

If your mortgage rate is ending within the next six months you should contact us to secure a new rate as soon as possible before your future options become more expensive

Halifax mortgage customers

- Existing Halifax borrower?

- Looking a Halifax mortgage renewal to a new mortgage product?

- Access rates lower than those on your App

- Looking for a Halifax 2-year fixed rate? – we can access 2-year rates for you

- Looking for the lowest Halifax renewal rates available for a +£250,000 mortgage?

- Check with our Team that you are being offered the best Halifax mortgage rate for your needs

- We answer our phone in seconds on 020 8979 9684

- Prefer to work online? Click here

7 Great Things about Halifax Product Transfers through A Mortgage Now

We can get you a lower remortgage rate

We can access lower Halifax Mortgage rates for larger mortgages that you cannot get directly from the Lender.

We can access ALL available Halifax rates for you

We establish your mortgage balance and current property value and let you know all the rates available to you (including two-year fixed rates which are not offered to you when you deal directly with Halifax).

You can reserve your new deal with us – now

You can reserve a new Halifax mortgage product up to four months (changed from six months August 2024) before your current deal ends. If your new Halifax rate is lower, we can even transfer your product early, saving you money.

You can switch quickly

We can get your new mortgage remortgage product offer secured within hours in most cases.

There’s no credit check

A Halifax product transfer is available regardless of your recent credit history.

Changes in your circumstances are not a problem

We can arrange a Halifax product transfer even if your income has dropped or one borrower has stopped working.

There’s no need for a house valuation

We obtain a valuation of your property from Halifax, the same day, at no cost.

We can arrange a re-mortgage if more appropriate

If the rates offered to you by Halifax do not suit you, we can place you with a more competitive lender.

Cancelling a product transfer request

if you no longer wish to proceed with a product transfer this can be cancelled at any time before it has taken effect. Once a product transfer has taken effect that cannot be cancelled and any early repayment charge on the product will be active,

Halifax referred to ‘completion’ of a product transfer, ‘completion’ is not the same as start date.

For example completion of a product transfer happens in the month before the new rate is due to start, if a rate has been future dated completion will be early in the month prior to the start date.

If an offer has been issued for product transfer to start the following month completion takes place shortly after the offer has been produced.

When completion takes place the borrower is sent to completion letter a few days later to confirm the new monthly payment.

Halifax indexed valuation

If you believe the Halifax index valuation figure is not accurate, it is possible to request a new valuation assessment. Under a new valuation assessment the valuation figure could be reduced as well as increased and borrowers should bear this in mind.

If improvement works have increased the floorspace of the property (extensions, loft conversions for example) a favourable new valuation is more likely.

Sub Accounts

Some Halifax borrowers will have sub accounts where they have had an initial loan and then raise extra against the loan is a further advance or as part of a house move. In these situations the two sub accounts can be on different product rate with different timings.

If a borrower has two separate products on their account ending within four months the option will be available to select the same new product that both product transfers. Where that new product carries a product fee, only one fee will be payable.

Interest Only?

If any part of your Halifax mortgage is on an interest only basis. We can still arrange your new Halifax mortgage rate for you. The process is a little more complex, but you will not notice as we manage those complications for you. All without any Broker Fees from us.

Halifax Product Transfers – Fee or no fee rate?

Halifax offers product transfer rates with and without product fees. On fee-charged mortgages the product fee is typically £999. The product fee may be paid upfront or added to your borrowing.

Why pay a product fee to Halifax?

The mortgage interest rates on fee-charged products can be considerably lower than the interest rates on products with no product fee. Therefore, for certain borrowers, your saving on interest when using a fee-paid product can easily outstrip the cost of the fee.

Simplified example: Borrowing is £200,000 fee is £999, the difference in interest rate between the fee and no fee rate is 0.2%. Over the term of a five-year product, you could be saving 0.2% per year in interest, over five years that totals 1% interest saved.

1% of £200,000 is £2,000, making the saving twice the cost of the £999 fee.

Why you should deal with a Broker?

There are a number of factors that can affect whether a fee-charged product is better for you. Factors such as:

- Your borrowing level

- Your mortgage term

- Overpayments

Therefore, making a decision on whether to use a fee-charged product can be complex and is best left to an experienced and regulated mortgage broker. This is not a call that Halifax want you to make without the proper advice, so they offer lower-interest products only via approved and regulated mortgage brokers such as A Mortgage Now.

Additional borrowing required?

We can help you arrange additional borrowing from Halifax at competitive rates for a number of reasons including:

- Home Improvements

- Extension

- Purchase adjacent land

- Extending your lease

- Gifts to relatives

- Purchase additional shares (affordable housing schemes)

- Buying out co-owner (e.g. ex Partner)

- Debt consolidation

- Buying further property (buy to let)

We handle the entire application process for you, and in most cases, the cash will be in your Bank account within 14 days.

Please note that satisfactory proof of income, and credit scoring will be required in order to increase your borrowing.

Minimum amount of additional borrowing is £5,000

Additional borrowing is not available within 6 months of completion of your mortgage

Account with arrears are not eligible for additional borrowing

Running a combined additional borrowing and product transfer application

If you are seeking to raise additional funds and also select a new product for your current borrowing this can be done in a single application. Once the additional funds have been drawn down, the product transfer will take effect from the first of the following month.

As a result if early repayment charges are currently active on the account are combined application needs to be keyed within the last four months of the existing product.

Moving home?

Are you intending to move home?

Are you aware that you may have the option to ‘port’ your current mortgage property when you move in order to avoid paying an early redemption penalty?

Halifax will allow you to take your current mortgage product with you and apply it to your new mortgage with any additional borrowing set up alongside a new rate.

Call us now for help with moving home.

Halifax mortgages with balances under £100,000?

Halifax does offer a set of new rates for mortgage borrowers with balances under £100,000. However, we do not usually assist in these cases.

Eligibility

In order to be eligible for Halifax Product Transfer switch:

- You must be an existing Halifax residential mortgage client

- Your mortgage account must be up-to-date with no history of arrears

- You must be currently on a product with a product end date in the next 90 days

Halifax ‘A’ Numbers Product Transfers

Have you a Halifax mortgage account number starting with an A?

Example

A/36575884-3

Have you been told you need to go in Branch to make a Product Transfer?

This is no longer the case and our team can assist you online.

Halifax is part of the Lloyds Banking Group and has the biggest market share on mortgages in the UK.

Halifax mortgage pricing is sometimes the most competitive in the market, but they do not seek to win business purely on price. Flexibility of their underwriting criteria is a key reason why many people use Halifax for their mortgage.

Below we outline some of the key points to note when considering Halifax as your mortgage provider.

Halifax underwriting – key benefits

Age

The maximum age at the end of the mortgage term with Halifax is 80 years. Where an applicant expects to take a mortgage beyond their retirement age, or age 70 (whichever is earlier), the lender will need to be confident that the applicant can support the mortgage on their proven retirement income.

The minimum age to obtain a mortgage with Halifax is 18 upon application.

Forces Help to Buy scheme

Funds from a Forces Help to Buy scheme can be used in conjunction with a Help to Buy scheme purchase.

Concessionary purchase

A concessionary purchase can be considered by Halifax, but only when the original owner moves out immediately on completion. The vendor can be a close family member or a landlord.

Gifted deposit from family

Gifted deposit is acceptable to Halifax from blood relatives or family by marriage or civil partnership, or between common-law partners or cohabitees.

They will not consider gifted deposits from friends, employers, landlords, or cousins.

Halifax and ‘mortgage prisoners’

Halifax will consider applicants classed as ‘mortgage prisoners’ for remortgage applications.

This applies to borrowers who found themselves with a mortgage lender that is no longer active and able to offer new rates.

Provided the applicant party’s credit score, Halifax can still accept the application even if affordability does not fit provided:

- it is a remortgage of the main residence with no additional borrowing

- maximum borrowing is 75% of the property value

- the new monthly payment must be no more than 5% higher than the current payment

- the mortgage cannot be on a shared equity or shared ownership scheme

- the potential borrowers must not be in financial difficulty*

*financial difficulty means failing current commitments of expenditure but not managing day-to-day control, overspending, overcommitted financially or over-indebted.

IT Contractors

Income from IT Contractors can be considered by Halifax where there is a 12-month history and six months of the contract remaining, or a two-year history as a contractor.

Multiple applicants

Halifax will accept up to 4 applicants considering a maximum of two incomes.

Professional sports people

Halifax will consider lending to professional sports people who have at least 12 months of employment with more than six months of their contract remaining. Where applicants are nearing the end of their likely careers the lender will want to satisfy themselves that monthly payments can be met should the career be ended abruptly due to injury.

Rental Income

Rental income can be used to offset the cost of buy-to-let mortgage payments but will not be added in to support affordability.

Remortgaging and raising capital

Halifax will consider remortgaging and raising of capital up to 85% loan to value.

Affordability and self-employment

Halifax currently offers slightly less unaffordability where one applicant is self-employed.

Applicants who own less than 25% of the business will not be considered self-employed for lending purposes and will be underwritten as employed.

Zero Hour contracts

Halifax will consider applicants with zero-hour contracts once they have a 12-month history.

Second Incomes

Halifax can accept income from a second job or self-employment provided they can satisfy themselves the client can sustain both forms of income.

Halifax underwriting – points to watch out for

Bankruptcy

Halifax will not consider applicants with a history of bankruptcy registered within the past six years.

EWS Forms

Halifax will require an external wall system form (EWS 1) where any building has a potentially combustible planning system. Full will need to confirm that there are no significant quantities of combustible materials or defects requiring remedial work. The valuer will advise where an EWS 1 form is required.

Buildings up to 6 stories or 18 m in height technically do not need at EWS 1 form but it may still be requested.

First Time Buyers

To be eligible for a first-time buyer product with Halifax at least one applicant needs to have not previously had a mortgage or purchased a property either in the UK or abroad.

Ex-Pats

Halifax does not accept applications from expats.

Interest only

Interest-only mortgages can be obtained with Halifax, but there are some strict criteria for eligibility.

In particular joint applicants must have a total income of £150,000 of a single applicant a total income of £100,000.

(Existing Halifax interest-only mortgage account holders are not subject to these criteria to continue on interest-only)

Where the sale of a mortgaged property is to be used as a method to repay the capital on the mortgage must be a minimum equity of £300,000. Lending up to 50% loan to value can be considered interest only with the remaining element up to 75% loan to value taken on a capital repayment basis.

Lending into retirement is not possible on an interest-only arrangement.

Halifax lending limits

Halifax will lend up to £500,000 with a 5% deposit, and up to £750,000 with a 10% deposit.

Borrowing over £1 million will require a minimum 20% deposit and a 30% deposit for borrowing over £2 million.

Maximum lending on remortgage of unencumbered policies will be 85% loan to value.

Lodgers

Up to 2 lodgers in the property are accepted provided they are sharing living accommodation. Income from lodgers is not included in affordability calculations.

Non-standard construction

Properties of non-standard construction can be considered and will be assessed on their own merits by the valuer. For example, precast concrete buildings may need to have undergone repair to be considered acceptable.

Halifax and self-build lending

Halifax will consider self-build lending but will need to schedule and cost of works, full planning consent, and appropriate insurance for construction.

Halifax customers cannot put their existing mortgage product into a self-build.

Maximum loan to value for self-build is 75% and loan size is up to £1 million.

Halifax will release the funds in a maximum of five instalments, normally at the following stages:

- purchase of the land

- completing the foundations

- construction of walls-to-wall plate level

- roof complete

- build complete

Lending on second homes

Halifax will consider lending on second homes up to 75% loan to value. Occasional letting of the second home can be considered but if more than four months per year it will be considered the buy-to-let and treated accordingly.

Halifax and leases

The minimum remaining lease term for a Halifax application is 70 years.

Minimum valuation

The minimum property valuation for Halifax applicants is £40,000

Mortgage Product Transfer with another Lender? – click below

- Accord Mortgages rates for existing Customers

- Aldermore Mortgages Loyalty Rates

- Barclays mortgage rates for existing customers

- Bluestone mortgage rates for existing customers

- BM Solutions Product Transfer rates

- Co Op Platform mortgages rates for existing customers

- Coventry Building Society new mortgage deals

- Godiva Mortgages Product Transfers

- HSBC Mortgage Customer Switching Rates

- Kensington Mortgages Product Transfers

- Kent Reliance Mortgage Product Transfer rates

- Leeds Building Society Product Transfer rates

- NatWest Mortgage switch deals

- Nationwide existing customers rate switch

- Newcastle BS existing customers rate switch

- Paragon Bank Mortgage Product Switch Service

- Pepper Money mortgages rates for existing customers

- Precise Product Transfers

- Santander Product Transfer rates

- Scottish Widows Bank Mortgage Product Transfer rates

- Skipton Mortgage Customer Switching Products

- The Mortgage Lender mortgage rates for existing customers

- The Mortgage Works | mortgage product switches for existing TMW buy to let borrowers

- Vida Homeloans mortgage rates for existing customers

- Virgin Money Mortgage Deals Existing Customers

Speak to our Team to find out more about how this works and how we can help you.